Summary

The market sentiment is very negative for mall real-estates.

Yet, fundamentals are quite resilient, especially for high-quality malls.

Malls are becoming mixed use real-estate as they redevelop and densify their properties. Winners will emerge in the coming years.

Low occupancy spaces along with the anticipated store closures makes the malls under pressure to deliver its promises to the investors. More specifically, it may lead to increased vacancy, lower NOI, higher capex needs and other releasing expenses in the near term.

How concerned should you be?

It depends. Over the short run, it adds to the uncertainty to all mall REITs. However, there are several risk-mitigating factors for REITs owning superior properties:

- Portfolio quality: The best malls in the nation are strong and replacement tenants should not be that challenging.

- Timing: Their malls are currently producing record high levels of sales and so the timing is perfect for releasing space.

- Low occupancy cost: The rents at many properties are currently below market – as evidenced by its historically low occupancy cost for many malls.

- Negotiation techniques: Whenever retailers file for store closure, they always go after the landlords for rent concessions. They scare them off with big plans of store closure, but this may or may not really be genuine in the end.

As of right now, we really do not know what the exact impact will be – but it’s fair to say that there will be a short-term hiccup. This hiccup is not however expected to be very significant with all things considered.

What’s more interesting to explore is what are the long-term implications of all these retail bankruptcies? The market is quick to jump to conclusions:

Retail bankruptcy = malls are dying…

We are much more optimistic than that. Malls offer many virtues that other retail channels are missing, and most importantly, malls have become “mixed use” destinations which assures long-term sustainability.

The Practicality of Malls

Something that we rarely discuss is why most shoppers still choose brick and mortar stores over e-commerce. In 2019, everybody knows about Amazon, Flipcart and others dominating the e-commerce for the youth. Yet, online sales remain only a small percentage of total retail sales.

Why is that? Well, think about it yourself. Why do you buy goods and services at malls? Most likely, it’s because of one of the following reasons:

- Immediate possession: You do not have to wait for shipping. You do not have to pay for it either.

- Physical inspection: You can touch, smell, try the product before making a decision.

- Advice and guidance: You are not on your own. You can ask questions to associates to guide you in your decision making.

- Social interactions: No one wants to sit at home in front of a computer to shop online after already working the whole day at the office.

- Showrooms: Whether it’s a Tesla, Apple, or even Amazon store, you get to see it before you buy it.

Put simply, there are a lot of reasons to shop at malls. We don’t do it because we have to. We do it because we prefer to. It’s the same reason why consumer spending on movie theaters and concerts keeps on growing – despite the rapid expansion of Netflix and Spotify :

Mixed-Use Destinations

Still to this day, when investors think of mall real-estate, they immediately think retail, high risk, store closures, and e-commerce. Even bulls like us are subconsciously affected by the constant flow of negative headlines.

In reality, there are no such thing as a “mall REIT” anymore. At least not in the sense that we used to know them in the past. Malls are not pure retail centers anymore. Malls have become “mixed use” destinations with a wide range of:

- Services (fitness, co-working, Amazon lockers, barber shops, repair shops, dry cleaning, hospital…)

- Entertainment (restaurants, bars, movie theaters, bowling, casinos,…)

- And Other Uses (Office space, apartments, hotels, storage,…)

What formerly used to be shopping destinations are now becoming much more versatile. Dying retailers are being replaced by other uses and properties are being densified with the addition of apartments, office and hotels on top of the mall and/or adjacent to it.

Is it working? You can be the judge…

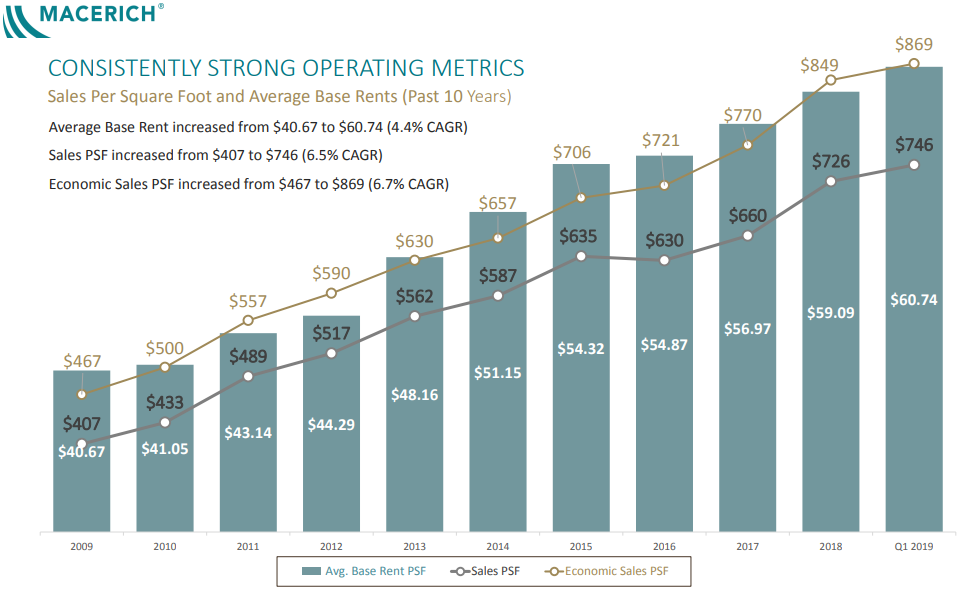

Sales per square foot have nearly doubled at many properties over the past 10 years – which is the same time period in which Amazon experienced enormous growth.

Clearly the mall transformation from “shopping” into “mixed use” is bearing its fruits. This is not debatable anymore at this point. It works so well because adding different uses benefits the entire mall economics. It brings greater and more consistent traffic. Think of a remote worker who visits a co-working spot at a mall, but then also ends up eating at a restaurant nearby and occasionally shops for clothes when he/she takes a break. Or someone who goes to the gym inside the mall, and then grabs a protein shake at the coffee shop and buys his sports gear next door. There are a lot of synergies in mixing the uses.

It also allows the mall to really focus on the stronger retailers – without any undue competition which would only cannibalize the total sales.

The above chart is the ultimate proof that the mixed use transformation is working. Will Amazon continue to grow? It sure will. But this does not mean much to a mall that has become a mixed use destination.

Retail Bankruptcies: Old News

Finally, I want to remind everyone that retail bankruptcies are nothing new. The market is connecting retail bankruptcies exclusively to the growth of e-commerce – when in reality, retail bankruptcies always have been a common occurrence. It’s simply part of business in an intensely competitive marketplace.

Retailers come and go…

R. Paul Drake posted an interesting report on the chat of High Yield Landlord recently that highlighted that too much debt and rapid over-expansion are the two main reasons for store closures over the past 2 years. In other words, e-commerce may have added fuel to the fire, but the real reason for these store closures is not purely e-commerce. The report adds that:

Lack of innovation and short-sighted private equity has also played a significant role. Retailers without these characteristics have continued to thrive, the report said, noting that when a retailer closes a lot of stores, it is more of an indictment on the individual retailer rather than an overall retail industry problem as has often been reported.

R. Paul Drake added on the chat that:

It looks to me like this wave of closings is more the usual story of a cycle of stupidity and greed than an apocalyptic societal change. I’ve wondered out loud before whether the slow growth of the present expansion might give time for waves of needed liquidation that delay the need for a next overall recession. That might perhaps be what is going on here.

Finally, while a lot of store closures are happening, it’s important to remember that for every retailer closing stores, there are more than five retail chains opening new ones – up from 3.7 in 2018.